Beneficial ownership requirements

Overview

This guidance came into force on June 1, 2021.

Beneficial ownership requirements under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and associated Regulations apply to all reporting entities (REs).

The concealment of beneficial ownership information is a technique used in money laundering and terrorist activity financing schemes. Identifying beneficial ownership removes the anonymity of the individuals behind the transactions and account activities, which is a key component of Canada's anti-money laundering and anti-terrorist financing regime. By collecting beneficial ownership information and confirming its accuracy, REs are performing an important step to mitigate the risk of money laundering and terrorist activity financing, and ultimately, to protect the integrity of Canada's financial system.

Who is this guidance for

- All reporting entities (REs)

In this guidance

- Who are beneficial owners?

- When must I obtain beneficial ownership information?

- When must I confirm the accuracy of beneficial ownership information?

- Are there circumstances where I do not have to obtain beneficial ownership information and confirm its accuracy?

- What beneficial ownership information do I need to obtain and confirm the accuracy of?

- How do I obtain the required beneficial ownership information?

- How do I confirm the accuracy of beneficial ownership information?

- What if I cannot obtain beneficial ownership information or confirm its accuracy?

- How do I verify the identity of an entity's chief executive officer or of the person who performs that function?

- What if there are no beneficial owners?

- What beneficial ownership records do I need to keep?

This guidance contains the following annexes, which provide examples of records for ownership, control and structure:

- Annex 1—Example of a record of beneficial ownership information for a corporation

- Annex 2—Example of a record of beneficial ownership information for an entity that is neither a corporation nor a trust

- Annex 3—Example of a record of beneficial ownership information for a trust (other than a widely held or publicly traded trust)

1. Who are beneficial owners?

Beneficial owners are the individuals who directly or indirectly own or control 25% or more of a corporation or an entity other than a corporation. In the case of a trust, they are the trustees, the known beneficiaries and the settlors of the trust. If the trust is a widely held trust or a publicly traded trust, they are the trustees and all persons who own or control, directly or indirectly, 25% or more of the units of the trust.Footnote 1

Beneficial owners cannot be other corporations, trusts or other entities. They must be the individuals who are the owners or controllers of the entity. It is important to consider and review the names found on official documentation in order to confirm the accuracy of the beneficial ownership information. It may be necessary to search through many layers of information in order to confirm who are the beneficial owners, as the names found on official documentation may not always reflect the actual beneficial owners.

2. When must I obtain beneficial ownership information?

You must obtain beneficial ownership information when you verify the identity of an entity in accordance with the Proceeds of Crime (Money Laundering) and Terrorist Financing Regulations (PCMLTFR).Footnote 2 For more information about when you are required to verify the identity of entities, see your sector's guidance on When to identify persons and entities.

The beneficial ownership information that you must obtain varies depending on whether the entity is a corporation, an entity other than a corporation (such as a partnership), a trust, or a widely held or publicly traded trust. The specific beneficial ownership information that you must obtain for each type of entity is detailed in section "5. What beneficial ownership information do I need to obtain and confirm the accuracy of?".

3. When must I confirm the accuracy of beneficial ownership information?

You must take reasonable measures to confirm the accuracy of the beneficial ownership information when you first obtain it and in the course of conducting ongoing monitoring of your business relationships.Footnote 3

4. Are there circumstances where I do not have to obtain beneficial ownership information and confirm its accuracy?

You do not have to obtain beneficial ownership information and take reasonable measures to confirm its accuracy in the following situations:

- For a group plan account held within a dividend or a distribution reinvestment plan. This includes plans that permits purchases of additional shares or units by the member with contributions other than the dividends or distributions paid by the plan sponsor, if the sponsor is an entity:Footnote 4

- whose shares or units are traded on a Canadian stock exchange; and

- that operates in a country that is a member of the Financial Action Task Force.

- If you are a financial entity, beneficial ownership requirements do not apply to your activities in respect of the processing of payments by credit card or prepaid payment product for a merchant.Footnote 5

- If you are a life insurance company, broker or agent, and you deal in reinsurance, beneficial ownership requirements do not apply to you for those dealings.Footnote 6

All RE sectors

The beneficial ownership requirements do not apply if you are not required to verify the identity of an entity under the Regulations because of a related exception. This is because your obligation to verify identity for a particular transaction, activity, or client does not apply in that circumstance.

5. What beneficial ownership information do I need to obtain and confirm the accuracy of?

When you verify an entity's identity in accordance with the PCMLTFR, you must obtain the following information about beneficial owners:Footnote 7

Corporations

- the names of all directors of the corporation and the names and addresses of all persons who directly or indirectly own or control 25% or more of the shares of the corporation.

Trusts

- the names and addresses of all trustees and all known beneficiaries and settlors of the trust.

Widely held or publicly traded trusts

- the names of all trustees of the trust and the names and addresses of all persons who directly or indirectly own or control 25% or more of the units of the trust.

Entities other than corporations or trusts

- the names and addresses of all persons who directly or indirectly own or control 25% or more of the entity.

In all cases, you must obtain information establishing the ownership, control and structure of the entity.Footnote 8

You must also take reasonable measures to confirm the accuracy of the information when you first obtain it and in the course of the ongoing monitoring of your business relationships.Footnote 9

If you verify the identity of a not-for-profit organization, you must also determine if the entity is:Footnote 10

- a charity registered with the Canada Revenue Agency under the Income Tax Act; or

- an organization, other than one referred to above, that solicits charitable donations from the public.

6. How do I obtain the required beneficial ownership information?

To obtain beneficial ownership information, which includes information on the ownership, control and structure, you could have the entity provide it, either verbally or in writing, or you could search for publicly available information.

For example:

- the entity can provide you with official documentation;

- the entity can tell you the beneficial ownership information and you can write it down for record keeping purposes; or

- the entity can fill out a document to provide you with the information.

7. How do I confirm the accuracy of beneficial ownership information?

You must take reasonable measures to confirm the accuracy of the beneficial ownership information that you obtain.Footnote 11 These reasonable measures cannot be the same as the measures you used to obtain the information.

Your reasonable measures could include referring to official documentation or records. For example, for a corporation or other entity, you could refer to records such as, but not limited to, the:

- minute book;

- securities register;

- shareholders register;

- articles of incorporation;

- annual returns;

- certificate of corporate status;

- shareholder agreements;

- partnership agreements; or

- board of directors' meeting records of decisions.

It is also acceptable to have a client sign a document to confirm the accuracy of the beneficial ownership information you obtained, which includes information on ownership, control and structure. In this case, it is possible for one document to be used to satisfy the two steps—namely to obtain the information and to confirm its accuracy by means of the signature.

In the case of a trust, you could confirm the accuracy of the information by reviewing the trust deed, which should provide you with the information needed.

Other reasonable measures can include:

- asking the client to provide supporting official documentation;

- conducting an open-source search; or

- consulting commercially available information.

As a best practice, you should also confirm whether a not-for-profit organization is a charity registered with the Canada Revenue Agency by consulting the charities listing on the Canada Revenue Agency website.

The reasonable measures that you take to confirm the accuracy of beneficial ownership information, which includes ownership, control, and structure information, must align with your risk assessment of the entity's risk for money laundering or terrorist activity financing offences. The reasonable measures you take with entities assessed to pose a high risk must go further to help you understand and confirm the beneficial ownership, as well as establish the overall ownership, control, and structure of that entity.

The reasonable measures that you take with entities that have a complex business structures must go further to ensure that you are able to understand and confirm the accuracy of beneficial ownership, which includes establishing the ownership, control and structure of that entity. This does not mean, however, that you need to consider or treat a complex entity as posing a high risk. You need to choose reasonable measures that are appropriate to the situation.

8. What if I cannot obtain beneficial ownership information or confirm its accuracy?

If you are unable to obtain the beneficial ownership information, to keep it up to date in the course of the ongoing monitoring of business relationships, or to confirm its accuracy, when it is first obtained, or during the course of ongoing monitoring then you must:Footnote 12

- take reasonable measures to verify the identity of the entity's chief executive officer or of the person who performs that function; and

- apply the special measures for high-risk clients, including enhanced ongoing monitoring.

For more information on enhanced ongoing monitoring, see FINTRAC's Ongoing monitoring requirements guidance.

9. How do I verify the identity of an entity's chief executive officer or of the person who performs that function?

The PCMLTFR does not require that you verify the identity of the chief executive officer or of the person who performs that function in accordance with the prescribed methods. However, you could use one of the methods outlined in the Methods to verify the identity of persons and entities guidance to meet this obligation.

Additionally, there is no record keeping obligation if you have identified the chief executive officer or a person who performs that function using the prescribed methods to verify identity. However, during a FINTRAC examination, you could be asked to demonstrate the reasonable measures that you took to identify the chief executive officer or person who performs that function.

10. What if there are no beneficial owners?

You may obtain information confirming that there is no individual who directly or indirectly owns or controls 25% or more of a corporation, a widely held or publicly traded trust, or an entity other than a corporation or trust. This is not the same thing as being unable to obtain the beneficial ownership information.

If you determine that there is no individual who directly or indirectly owns or controls 25% or more of a corporation, a widely held or publicly traded trust, or an entity other than a corporation or trust, you must keep a record of the measures you took and the information you obtained in order to reach that conclusion.Footnote 13 However, you are still required to obtain and take reasonable measures to confirm information about the ownership, control and structure of the entity.

11. What beneficial ownership records do I need to keep?

You must keep a record of the beneficial ownership information you obtain and of the measures you take to confirm the accuracy of the information.Footnote 14

The measures that you take to confirm beneficial ownership information can be part of your overall policies and procedures, so a separate record may not be needed. You only need to keep an individual record of the specific measures you take to confirm the accuracy of beneficial ownership information in situations where the measures differ from those that are documented in your policies and procedures.

For a corporation, you must record:Footnote 15

- the names of all directors of the corporation;

- the names and addresses of all persons who directly or indirectly own or control 25% or more of the shares of the corporation; and

- information establishing the ownership, control and structure of the corporation.

For a trust, you must record:Footnote 16

- the names and addresses of all trustees, known beneficiaries and known settlors of the trust; and

- information establishing the ownership, control and structure of the trust.

For a widely held or publicly traded trust, you must record:Footnote 17

- the names of all trustees of the trust;

- the names and addresses of all persons who directly or indirectly own or control 25% or more of the units of the trust; and

- information establishing the ownership, control and structure of the trust.

For an entity other than a corporation or trust, you must record:Footnote 18

- the names and addresses of all persons who directly or indirectly own or control 25% or more of the entity; and

- information establishing the ownership, control and structure of the entity.

If you verify the identity of a not-for-profit organization, you must also keep a record that indicates whether the entity is:Footnote 19

- a charity registered with the Canada Revenue Agency under the Income Tax Act; or

- an organization, other than a registered charity, that solicits charitable donations from the public.

In situations where no individual directly or indirectly owns or controls 25% or more of a corporation, a widely held or publicly traded trust, or an entity other than a corporation or trust, you must keep a record of the measures you took to confirm the accuracy of the information, as well as the information you obtained in order to reach that conclusion. The date you took the measures should also be included as a best practice.

Retention: You must keep these records for at least five years from the day the last business transaction is conducted.Footnote 20

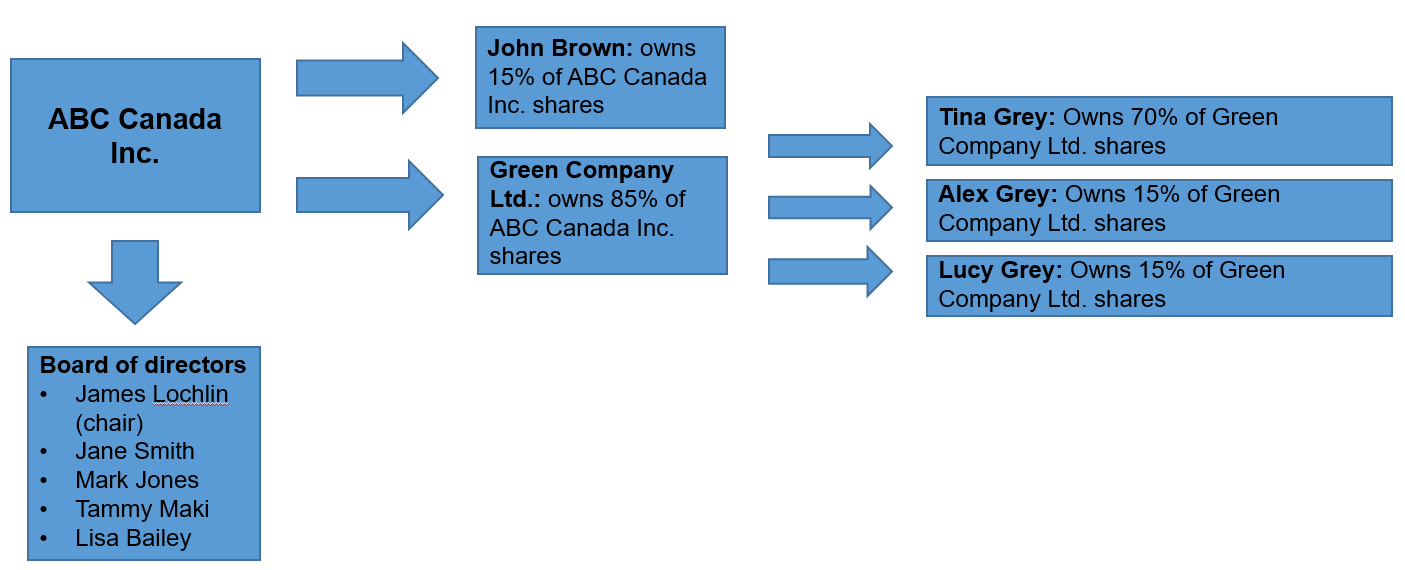

Annex 1—Example of a record of beneficial ownership information for a corporation

Scenario:

ABC Canada Inc., a privately held corporation incorporated under the Canada Business Corporations Act, carries out a transaction or activity for which you have to verify its identity, triggering your beneficial ownership obligations. You learn that ABC Canada Inc. is owned by John Brown and Green Company Ltd. You discover that John owns 15% of the shares in the company (15 of the 100 total) and that Green Company Ltd. owns 85% of the shares (85 of 100 total). Since Green Company Ltd. owns and controls more than 25% of ABC Canada Inc., you need to find the beneficial owners, who cannot be a corporation or an entity. You inquire further and discover that Tina Grey owns 70% of Green Company Inc.'s shares and her two children, Alex and Lucy Grey, each own 15% respectively. Next, you learn that ABC Canada Inc.'s board of directors is made up of:

- James Lochlin, Chair;

- Jane Smith, Chief Financial Officer;

- Mark Jones, director;

- Tammy Maki, director; and

- Lisa Bailey, director.

Diagram 1—Beneficial ownership information for a corporation

In this example, you must record:

- The names of all directors of ABC Canada Inc.:

- James Lochlin (chair);

- Jane Smith;

- Mark Jones;

- Tammy Maki; and

- Lisa Bailey.

- The names and addresses of all of the persons who directly or indirectly own or control 25% or more of the shares of ABC Canada Inc.:

- The name and address of Tina Grey, who owns 70% of Green Company Ltd. Since Green Company Ltd. owns 85% of ABC Canada Inc.'s shares, and Tina owns 70% of Green Company Ltd.'s shares, Tina indirectly owns and controls more than 25% of the shares of ABC Canada Inc.

- The information establishing the ownership, control and structure of ABC Canada Inc., including:

- the ownership of ABC Canada Inc. being shared between John Brown (15%) and Green Company Ltd. (85%);

- the ownership of Green Company Ltd. being shared between Tina Grey (70%), Alex Grey (15%), and Lucy Grey (15%);

- the control of ABC Canada Inc. significantly being held by Green Company Ltd. and specifically Tina Grey (who indirectly owns and controls more than 25% of ABC Canada Inc.'s shares);

- the structure of ABC Canada Inc., including that it is a privately held corporation, and

- other structure details about ABC Canada Inc., including the positions held by each director and any organization chart.

- The reasonable measures you took to confirm the accuracy of the information:

- the steps you took as reasonable measures to confirm the accuracy of this information; and

- any official documents obtained to support the measures you took.

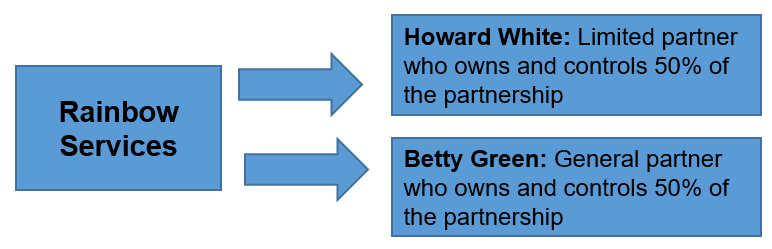

Annex 2—Example of a record of beneficial ownership information for an entity that is neither a corporation nor a trust

Scenario:

Rainbow Services, a partnership, carries out a transaction or activity for which you have to verify its identity, thus triggering your beneficial ownership obligations. You learn that Howard White and Betty Green are the two partners in this partnership. Betty is the general partner and is responsible for operating the day-to-day operations and Howard is the limited partner who has invested funds into the partnership. All decisions related to the partnership must be unanimous, and either partner can decide to end the partnership.

Diagram 2—Beneficial ownership information for an entity that is neither a corporation nor a trust

In this example you must record:

- The names and addresses of all persons who directly or indirectly own or control 25% or more of Rainbow Services:

- Howard and Betty's names and addresses, as the partners who equally own and control the partnership.

- The information establishing the ownership, control and structure of Rainbow Services, including that:

- the ownership and control of Rainbow Services is held equally between Howard (50%) and Betty (50%), the structure of Rainbow Services, including that it is a partnership between Howard and Betty, and

- any other structure details about Rainbow Services, including any organizational chart.

- The reasonable measures you took to confirm the accuracy of the information:

- the steps you took as reasonable measures to confirm the accuracy of this information; and

- any official documents obtained to support the measures you took, such as a copy of the partnership agreement.

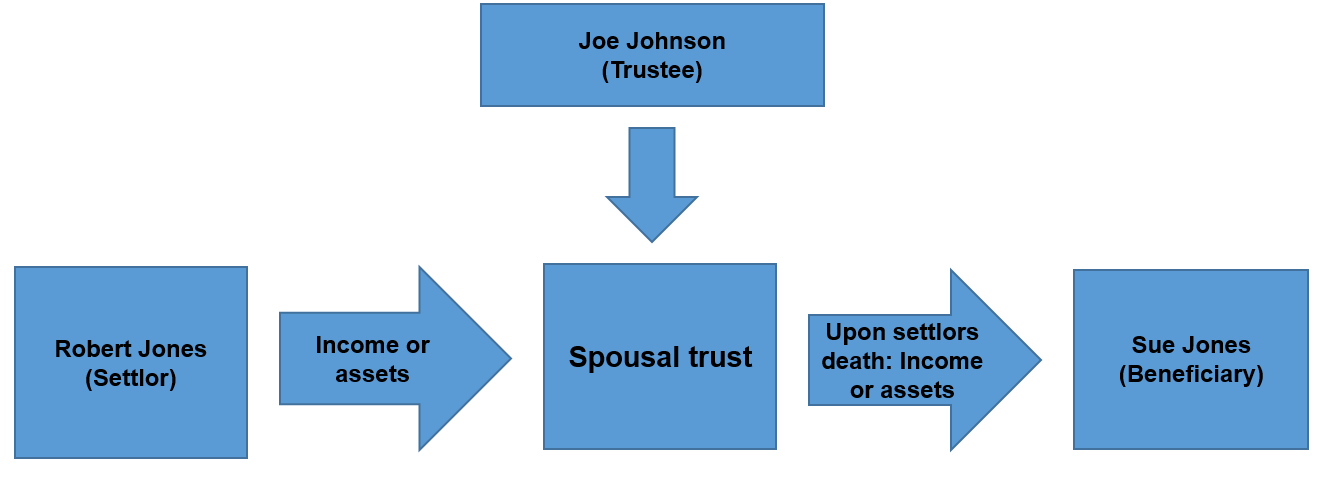

Annex 3—Example of a record of beneficial ownership information for a trust (other than a widely held or publicly traded trust)

Scenario:

A trust carries out a transaction or activity for which you are required to verify its identity, triggering your beneficial ownership obligations. You learn that Robert Jones established a spousal trust for his wife Sue. He transferred assets into the trust and designated Joe Johnson as the trustee.

Diagram 3—Beneficial ownership information for a trust (other than a widely held or publicly traded trust)

In this example you must record:

- The names and addresses of all trustees, known beneficiaries and known settlors of the trust:

- Robert's name and address, as he is the settlor;

- Joe's name and address, as he is trustee; and

- Sue's name and address, as she is the beneficiary.

- The information establishing the ownership, control and structure of the trust, including:

- The beneficial ownership information is reflected in the information required to be obtained for the trust:

- Robert is the settlor and can modify or revoke the terms of the trust;

- Joe is the trustee and controls the assets in the trust; and

- Sue, as the beneficiary, is the only person entitled to receive the assets or income from the trust.

- The structure of the trust, including that it is a spousal trust.

- The beneficial ownership information is reflected in the information required to be obtained for the trust:

- The reasonable measures you took to confirm the accuracy of the information:

- the steps you took as reasonable measures to confirm the accuracy of this information; and

- any official documents obtained to support the measures you took, such as the trust agreement.

Details and history

Published: March 2021

For assistance

If you have questions about this guidance, please contact FINTRAC by email at guidelines-lignesdirectrices@fintrac-canafe.gc.ca.

Definitions

- Accountant

A chartered accountant, a certified general accountant, a certified management accountant or, if applicable, a chartered professional accountant. (comptable)

Reference:

Proceeds of Crime (Money Laundering) and Terrorist Financing Regulations (PCMLTFR), SOR/2002-184, s. 1(2).- Accounting firm

An entity that is engaged in the business of providing accounting services to the public and has at least one partner, employee or administrator that is an accountant. (cabinet d'expertise comptable)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Act

The Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA). (la Loi)

Reference:

Proceeds of Crime (Money Laundering) and Terrorist Financing Administrative Monetary Penalties Regulations (PCMLTFAMPR), SOR/2007-292, s. 1, Proceeds of Crime (Money Laundering) and Terrorist Financing Registration Regulations (PCMLTFRR), SOR/2007-121, s. 1, PCMLTFR, SOR/2002-184, s. 1(2), and Proceeds of Crime (Money Laundering) and Terrorist Financing Suspicious Transaction Reporting Regulations (PCMLTFSTRR), SOR/2001-317, s. 1(2).- Administrative monetary penalties (AMPs)

Civil penalties that may be issued to reporting entities by FINTRAC for non-compliance with the PCMLTFA and associated Regulations. (pénalité administrative pécuniaire [PAP])

- Affiliate

An entity is affiliated with another entity if one of them is wholly owned by the other, if both are wholly owned by the same entity or if their financial statements are consolidated. (entité du même groupe)

Reference:

PCMLTFR, SOR/2002-184, s. 4.- Annuity

Has the same meaning as in subsection 248(1) of the Income Tax Act. (rente)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- As soon as practicable

A time period that falls in-between immediately and as soon as possible, within which a suspicious transaction report (STR) must be submitted to FINTRAC. The completion and submission of the STR should take priority over other tasks. In this context, the report must be completed promptly, taking into account the facts and circumstances of the situation. While some delay is permitted, it must have a reasonable explanation. (aussitôt que possible)

- Attempted transaction

Occurs when an individual or entity starts to conduct a transaction that is not completed. For example, a client or a potential client walks away from conducting a $10,000 cash deposit. (opération tentée)

- Authentic

In respect of verifying identity, means genuine and having the character of an original, credible, and reliable document or record. (authentique)

- Authorized person

A person who is authorized under subsection 45(2). (personne autorisée)

Reference:

Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA), S.C. 2000, c 17, s. 2(1).- Authorized user

A person who is authorized by a holder of a prepaid payment product account to have electronic access to funds or virtual currency available in the account by means of a prepaid payment product that is connected to it. (utilisateur autorisé)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Beneficial owner(s)

Beneficial owners are the individuals who are the trustees, and known beneficiaries and settlors of a trust, or who directly or indirectly own or control 25% or more of i) the shares of a corporation or ii) an entity other than a corporation or trust, such as a partnership. The ultimate beneficial owner(s) cannot be another corporation or entity; it must be the actual individual(s) who owns or controls the entity. (bénéficiaire effectif)

- Beneficiary

A beneficiary is the individual or entity that will benefit from a transaction or to which the final remittance is made. (bénéficiaire)

- Branch

A branch is a part of your business at a distinct location other than your main office. (succursale)

- British Columbia notary corporation

An entity that carries on the business of providing notary services to the public in British Columbia in accordance with the Notaries Act, R.S.B.C. 1996, c. 334. (société de notaires de la Colombie-Britannique)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- British Columbia notary public

A person who is a member of the Society of Notaries Public of British Columbia. (notaire public de la Colombie-Britannique)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Cash

Coins referred to in section 7 of the Currency Act, notes issued by the Bank of Canada under the Bank of Canada Act that are intended for circulation in Canada or coins or bank notes of countries other than Canada. (espèces)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2) and PCMLTFSTRR, SOR/2001-317, s. 1(2).- Casino

A government, organization, board or operator that is referred to in any of paragraphs 5(k) to (k.3) of the Act. (casino)

Reference:

PCMLTFR, SOR/2002-184, s 1(2) and PCMLTFSTRR, SOR/2001-317, s. 1(2).- Certified translator

An individual that holds the title of professional certified translator granted by a Canadian provincial or territorial association or body that is competent under Canadian provincial or territorial law to issue such certification. (traducteur agréé)

- Clarification request

A clarification request is a method used to communicate with money services businesses (MSBs) or foreign money services businesses (FMSBs) when FINTRAC needs more information about their registration form. This request is usually sent by email. (demande de précisions)

- Client

A person or entity that engages in a financial transaction with another person or entity. (client)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Client identification information

The identifying information that you have obtained on your clients, such as name, address, telephone number, occupation or nature of principal business, and date of birth for an individual. (renseignements d'identification du client)

- Competent authority

For the purpose of the criminal record check submitted with an application for registration, a competent authority is any person or organization that has the legally delegated or invested authority, capacity, or power to issue criminal record checks. (autorité compétente)

- Completed transaction

Is a transaction conducted by a person or entity, that is completed and results in the movement of funds, virtual currency, or the purchase or sale of an asset. (opération effectuée)

- Completing action

With respect to a reportable transaction, information related to the instructions provided by the person or entity making the request to the reporting entity to complete a transaction. For example, an individual arrives at a bank and requests to purchase a bank draft. The completing action is the details of how the reporting entity fulfilled the person or entity’s instructions which led to the transaction being completed. This includes what the funds or virtual currency initially brought to the reporting entity was used for (see “disposition”). A transaction may have one or more completing actions depending on the instructions provided by the person or entity. (action d’achèvement)

- Compliance officer

The individual, with the necessary authority, that you appoint to be responsible for the implementation of your compliance program. (agent de conformité)

- Compliance policies and procedures

Written methodology outlining the obligations applicable to your business under the PCMLTFA and its associated Regulations and the corresponding processes and controls you put in place to address your obligations. (politiques et procédures de conformité)

- Compliance program

All elements (compliance officer, policies and procedures, risk assessment, training program, effectiveness review) that you, as a reporting entity, are legally required to have under the PCMLTFA and its associated Regulations to ensure that you meet all your obligations. (programme de conformité)

- Context

Clarifies a set of circumstances or provides an explanation of a situation or financial transaction that can be understood and assessed. (contexte)

- Correspondent banking relationship

A relationship created by an agreement or arrangement under which an entity referred to in any of paragraphs 5(a), (b), (d),(e) and (e.1) or an entity that is referred to in section 5 and that is prescribed undertakes to provide to a prescribed foreign entity prescribed services or international electronic funds transfers, cash management or cheque clearing services. (relation de correspondant bancaire)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 9.4(3) and PCMLTFR, SOR/2002-184, s. 16(1)(b).- Country of residence

The country where an individual has lived continuously for 12 months or more. The individual must have a dwelling in the country concerned. For greater certainty, a person only has one country of residence no matter how many dwelling places they may have, inside or outside of that country. (pays de résidence)

- Credit card acquiring business

A credit card acquiring business is a financial entity that has an agreement with a merchant to provide the following services:

- enabling a merchant to accept credit card payments by cardholders for goods and services and to receive payments for credit card purchases;

- processing services, payment settlements and providing point-of-sale equipment (such as computer terminals); and

- providing other ancillary services to the merchant.

- Credit union central

A central cooperative credit society, as defined in section 2 of the Cooperative Credit Associations Act, or a credit union central or a federation of credit unions or caisses populaires that is regulated by a provincial Act other than one enacted by the legislature of Quebec. (centrale de caisses de crédit)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Crowdfunding platform

A website or an application or other software that is used to raise funds or virtual currency through donations. (plateforme de sociofinancement)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Crowdfunding platform services

The provision and maintenance of a crowdfunding platform for use by other persons or entities to raise funds or virtual currency for themselves or for persons or entities specified by them. (services de plateforme de sociofinancement)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Current

In respect of a document or source of information that is used to verify identity, is up to date, and, in the case of a government-issued photo identification document, must not have been expired when the ID was verified. (à jour)

- Dealer in precious metals and stones

A person or entity that, in the course of their business activities, buys or sells precious metals, precious stones or jewellery. It includes a department or an agent of His Majesty in right of Canada or an agent or mandatary of His Majesty in right of a province when the department or the agent or mandatary carries out the activity, referred to in subsection 65(1), of selling precious metals to the public. (négociant en métaux précieux et pierres précieuses)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Deferred profit sharing plan

Has the same meaning as in subsection 248(1) of the Income Tax Act. (régime de participation différée aux bénéfices)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Deposit slip

A record that sets out:

- (a) the date of the deposit;

- (b) the name of the person or entity that makes the deposit;

- (c) the amount of the deposit and of any part of it that is made in cash;

- (d) the method by which the deposit is made; and

- (e) the number of the account into which the deposit is made and the name of each account holder.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Directing services

A business is directing services at persons or entities in Canada if at least one of the following applies:

- The business's marketing or advertising is directed at persons or entities located in Canada;

- The business operates a ".ca" domain name; or,

- The business is listed in a Canadian business directory.

Additional criteria may be considered, such as if the business describes its services being offered in Canada or actively seeks feedback from persons or entities in Canada. (diriger des services)

- Distributed ledger

For the purpose of section 151 of the Proceeds of Crime (Money Laundering) and Terrorist Financing Regulations (PCMLTFR), a digital ledger that is maintained by multiple persons or entities and that can only be modified by a consensus of those persons or entities. (registres distribués)

Reference:

PCMLTFR, SOR/2002-184, s. 151(2).- Disposition

With respect to a reportable transaction, the disposition is what the funds or virtual currency was used for. For example, an individual arrives at a bank with cash and purchases a bank draft. The disposition is the purchase of the bank draft. (répartition)

- Electronic funds transfer

The transmission—by any electronic, magnetic or optical means—of instructions for the transfer of funds, including a transmission of instructions that is initiated and finally received by the same person or entity. In the case of SWIFT messages, only SWIFT MT-103 messages and their equivalent are included. It does not include a transmission or instructions for the transfer of funds:

- (a) that involves the beneficiary withdrawing cash from their account;

- (b) that is carried out by means of a direct deposit or pre-authorized debit;

- (c) that is carried out by cheque imaging and presentment

- (d) that is both initiated and finally received by persons or entities that are acting to clear or settle payment obligations between themselves; or

- (e) that is initiated or finally received by a person or entity referred to in paragraphs 5(a) to (h.1) of the Act for the purpose of internal treasury management, including the management of their financial assets and liabilities, if one of the parties to the transaction is a subsidiary of the other or if they are subsidiaries of the same corporation.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Employees profit sharing plan

Has the same meaning as in subsection 248(1) of the Income Tax Act. (régime de participation des employés aux bénéfices)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Entity

A body corporate, a trust, a partnership, a fund or an unincorporated association or organization. (entité)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Facts

Actual events, actions, occurrences or elements that exist or are known to have happened or existed. Facts are not opinions. For example, facts surrounding a transaction or multiple transactions could include the date, time, location, amount or type of transaction or could include the account details, particular business lines, or the client's financial history. (faits)

- Family member

For the purposes of subsection 9.3(1) of the Act, a prescribed family member of a politically exposed foreign person, a politically exposed domestic person or a head of an international organization is:

- (a) their spouse or common-law partner;

- (b) their child;

- (c) their mother or father;

- (d) the mother or father of their spouse or common-law partner; or

- (e) a child of their mother or father.

Reference:

PCMLTFR, SOR/2002-184, s. 2(1).- Fiat currency

A currency that is issued by a country and is designated as legal tender in that country. (monnaie fiduciaire)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2) and PCMLTFSTRR, SOR/2001-317, s. 1(2).- Final receipt

In respect of an electronic funds transfer, means the receipt of the instructions by the person or entity that is to make the remittance to a beneficiary. (destinataire)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Financial entity

Means:

- (a) an entity that is referred to in any of paragraphs 5(a), (b) and (d) to (f) of the Act;

- (b) a financial services cooperative;

- (c) a life insurance company, or an entity that is a life insurance broker or agent, in respect of loans or prepaid payment products that it offers to the public and accounts that it maintains with respect to those loans or prepaid payment products, other than:

- (i) loans that are made by the insurer to a policy holder if the insured person has a terminal illness that significantly reduces their life expectancy and the loan is secured by the value of an insurance policy;

- (ii) loans that are made by the insurer to the policy holder for the sole purpose of funding the life insurance policy; and

- (iii) advance payments to which the policy holder is entitles that are made to them by the insurer;

- (d) a credit union central when it offers financial services to a person, or to an entity that is not a member of that credit union central; and

- (e) a department, or an entity that is an agent of His Majesty in right of Canada or an agent or mandatary of His Majesty in right of a province, when it carries out an activity referred to in section 76.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Financial Action Task Force

The Financial Action Task Force on Money Laundering established in 1989. (Groupe d'action financière)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Financial services cooperative

A financial services cooperative that is regulated by an Act respecting financial services cooperatives, CQLR, c. C-67.3, other than a caisse populaire. (coopérative de services financiers)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Foreign currency

A fiat currency that is issued by a country other than Canada. (devise)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Foreign currency exchange transaction

An exchange, at the request of another person or entity, of one fiat currency for another. (opération de change en devise)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Foreign currency exchange transaction ticket

A record respecting a foreign currency exchange transaction—including an entry in a transaction register—that sets out:

- (a) the date of the transaction;

- (b) in the case of a transaction of $3,000 or more, the name and address of the person or entity that requests the exchange, the nature of their principal business or their occupation and, in the case of a person, their date of birth;

- (c) the type and amount of each of the fiat currencies involved in the payment made and received by the person or entity that requests the exchange;

- (d) the method by which the payment is made and received;

- (e) the exchange rates used and their source;

- (f) the number of every account that is affected by the transaction, the type of account and the name of each account holder; and

- (g) every reference number that is connected to the transaction and has a function equivalent to that of an account number.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Foreign money services business

Persons and entities that do not have a place of business in Canada, that are engaged in the business of providing at least one of the following services that is directed at persons or entities in Canada, and that provide those services to their clients in Canada:

- (i) foreign exchange dealing,

- (ii) remitting funds or transmitting funds by any means or through any person, entity or electronic funds transfer network,

- (iii) issuing or redeeming money orders, traveller's cheques or other similar negotiable instruments except for cheques payable to a named person or entity,

- (iv) dealing in virtual currencies, or

- (v) any prescribed service.

Reference:

PCMLTFA, S.C. 2000, c 17, s. 5(h.1), PCMLTFRR, SOR/2007-121, s. 1 and PCMLTFR, SOR/2002-184, s. 1(2).- Foreign state

Except for the purposes of Part 2, means a country other than Canada and includes any political subdivision or territory of a foreign state. (État étranger)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Funds

Means:

- (a) cash and other fiat currencies, and securities, negotiable instruments or other financial instruments that indicate a title or right to or interest in them; or

- (b) a private key of a cryptographic system that enables a person or entity to have access to a fiat currency other than cash.

For greater certainty, it does not include virtual currency. (fonds)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2) and PCMLTFSTRR, SOR/2001-317, s. 1(2).- Head of an international organization

A person who, at a given time, holds—or has held within a prescribed period before that time—the office or position of head of

- a) an international organization that is established by the governments of states;

- b) an institution of an organization referred to in paragraph (a); or

- c) an international sports organization.

Reference:

PCMLTFA, S.C. 2000, c 17, s. 9.3(3).- Immediately

In respect of submitting a Terrorist Property Report (TPR), the time period within which a TPR must be submitted, which does not allow for any delay prior to submission. (immédiatement)

- Information record

A record that sets out the name and address of a person or entity and:

- (a) in the case of a person, their date of birth and the nature of their principal business or their occupation; and

- (b) in the case of an entity, the nature of its principal business.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Initiation

In respect of an electronic funds transfer, means the first transmission of the instructions for the transfer of funds. (amorcer)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Institutional trust

For the purpose of section 15 of the Proceeds of Crime (Money Laundering) and Terrorist Financing Regulations (PCMLTFR), means a trust that is established by a corporation or other entity for a particular business purpose and includes a pension plan trust, a pension master trust, a supplemental pension plan trust, a mutual fund trust, a pooled fund trust, a registered retirement savings plan trust, a registered retirement income fund trust, a registered education savings plan trust, a group registered retirement savings plan trust, a deferred profit sharing plan trust, an employee profit sharing plan trust, a retirement compensation arrangement trust, an employee savings plan trust, a health and welfare trust, an unemployment benefit plan trust, a foreign insurance company trust, a foreign reinsurance trust, a reinsurance trust, a real estate investment trust, an environmental trust and a trust established in respect of endowment, a foundation or a registered charity. (fiducie institutionnelle)

Reference:

PCMLTFR, SOR/2002-184, s. 15(2).- International electronic funds transfer

An electronic funds transfer other than for the transfer of funds within Canada. (télévirement international)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Inter vivos trust

A personal trust, other than a trust created by will. (fiducie entre vifs)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Jewellery

Objects that are made of gold, silver, palladium, platinum, pearls or precious stones and that are intended to be worn as a personal adornment. (bijou)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Large cash transaction record

A record that indicates the receipt of an amount of $10,000 or more in cash in a single transaction and that contains the following information:

- (a) the date of the receipt;

- (b) if the amount is received for deposit into an account, the number of the account, the name of each account holder and the time of the deposit or an indication that the deposit is made in a night deposit box outside the recipient's normal business hours;

- (c) the name and address of every other person or entity that is involved in the transaction, the nature of their principal business or their occupation and, in the case of a person, their date of birth;

- (d) the type and amount of each fiat currency involved in the receipt;

- (e) the method by which the cash is received;

- (f) if applicable, the exchange rates used and their source;

- (g) the number of every other account that is affected by the transaction, the type of account and the name of each account holder

- (h) every reference number that is connected to the transaction and has a function equivalent to that of an account number;

- (i) the purpose of the transaction;

- (j) the following details of the remittance of, or in exchange for, the cash received:

- (i) the method of remittance;

- (ii) if the remittance is in funds, the type and amount of each type of funds involved;

- (iii) if the remittance is not in funds, the type of remittance and its value, if different from the amount of cash received; and

- (iv) the name of every person or entity involved in the remittance and their account number or policy number or, if they have no account number or policy number, their identifying number; and

- (k) if the amount is received by a dealer in precious metals and precious stones for the sale of precious metals, precious stones or jewellery:

- (i) the type of precious metals, precious stones or jewellery;

- (ii) the value of the precious metals, precious stones or jewellery, if different from the amount of cash received, and

- (iii) the wholesale value of the precious metals, precious stones or jewellery.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Large virtual currency transaction record

A record that indicates the receipt of an amount of $10,000 or more in virtual currency in a single transaction and that contains the following information:

- (a) the date of the receipt;

- (b) if the amount is received for deposit into an account, the name of each account holder;

- (c) the name and address of every other person or entity that is involved in the transaction, the nature of their principal business or their occupation and, in the case of a person, their date of birth;

- (d) the type and amount of each virtual currency involved in the receipt;

- (e) the exchange rates used and their source;

- (f) the number of every other account that is affected by the transaction, the type of account and the name of each account holder;

- (g) every reference number that is connected to the transaction and has a function equivalent to that of an account number;

- (h) every transaction identifier, including the sending and receiving addresses; and

- (i) if the amount is received by a dealer in precious metals and precious stones for the sale of precious metals, precious stones or jewellery:

- (i) the type of precious metals, precious stones or jewellery;

- (ii) the value of the precious metals, precious stones or jewellery, if different from the amount of virtual currency received; and

- (iii) the wholesale value of the precious metals, precious stones or jewellery.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Life insurance broker or agent

A person or entity that is authorized under provincial legislation to carry on the business of arranging contracts of life insurance. (représentant d'assurance-vie)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Life insurance company

A life company or foreign life company to which the Insurance Companies Act applies or a life insurance company regulated by a provincial Act. (société d'assurance-vie)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Listed person

Has the same meaning as in section 1 of the Regulations Implementing the United Nations Resolutions on the Suppression of Terrorism. (personne inscrite)

Reference:

PCMLTFSTRR, SOR/2001-317, s. 1(2).- Managing general agents (MGAs)

Life insurance brokers or agents that act as facilitators between other life insurance brokers or agents and life insurance companies. MGAs typically offer services to assist with insurance agents contracting and commission payments, facilitate the flow of information between insurer and agent, and provide training to, and compliance oversight of, insurance agents. (agent général de gestion)

- Mandatary

A person who acts, under a mandate or agreement, for another person or entity. (mandataire)

- Marketing or advertising

When a person or entity uses promotional materials such as advertisements, graphics for websites or billboards, etc., with the intent to promote money services business (MSB) services and to acquire business from persons or entities in Canada. (marketing ou publicité)

- Minister

In relation to sections 24.1 to 39, the Minister of Public Safety and Emergency Preparedness and, in relation to any other provision of this Act, the Minister of Finance. (ministre)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Money laundering offence

An offence under subsection 462.31(1) of the Criminal Code. The United Nations defines money laundering as "any act or attempted act to disguise the source of money or assets derived from criminal activity." Essentially, money laundering is the process whereby "dirty money"—produced through criminal activity—is transformed into "clean money," the criminal origin of which is difficult to trace. (infraction de recyclage des produits de la criminalité)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Money laundering and terrorist financing indicators (ML/TF indicators)

Potential red flags that could initiate suspicion or indicate that something may be unusual in the absence of a reasonable explanation. [Indicateurs de blanchiment d'argent (BA) et de financement du terrorisme (FT) (indicateurs de BA/FT)]

- Money services business

A person or entity that has a place of business in Canada and that is engaged in the business of providing at least one of the following services:

- (i) foreign exchange dealing,

- (ii) remitting funds or transmitting funds by any means or through any person, entity or electronic funds transfer network,

- (iii) issuing or redeeming money orders, traveller's cheques or other similar negotiable instruments except for cheques payable to a named person or entity,

- (iv) dealing in virtual currencies, or

- (v) any prescribed service.

Reference:

PCMLTFA, S.C. 2000, c 17, s. 5(h), PCMLTFRR, SOR/2007-121, s. 1 and PCMLTFR, SOR/2002-184, s. 1(2).- Money services business agent

An individual or entity authorized to deliver services on behalf of a money services business (MSB). It is not an MSB branch. (mandataire d'une entreprise de services monétaires)

- Nature of principal business

An entity's type or field of business. Also applies to an individual in the case of a sole proprietorship. (nature de l'entreprise principale)

- New developments

Changes to the structure or operations of a business when new services, activities, or locations are put in place. For example, changes to a business model or business restructuring. (nouveaux développements)

- New technologies

The adoption of a technology that is new to a business. For example, when a business adopts new systems or software such as transaction monitoring systems or client onboarding and identification tools. (nouvelles technologies)

- No apparent reason

There is no clear explanation to account for suspicious behaviour or information. (sans raison apparente)

- Occupation

The job or profession of an individual. (profession ou métier)

- Person

An individual. (personne)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Person authorized to give instructions

In respect of an account, means a person who is authorized to instruct on the account or make changes to the account, such as modifying the account type, updating the account contact details, and in the case of a credit card account, requesting a limit increase or decrease, or adding or removing card holders. A person who is only able to conduct transactions on the account is not considered a person authorized to give instructions. (personne habilitée à donner des instructions)

- Politically exposed domestic person

A person who, at a given time, holds—or has held within a prescribed period before that time—one of the offices or positions referred to in any of paragraphs (a) and (c) to (j) in or on behalf of the federal government or a provincial government or any of the offices or positions referred to in paragraphs (b) and (k):

- (a) Governor General, lieutenant governor or head of government;

- (b) member of the Senate or House of Commons or member of a legislature of a province;

- (c) deputy minister or equivalent rank;

- (d) ambassador, or attaché or counsellor of an ambassador;

- (e) military officer with a rank of general or above;

- (f) president of a corporation that is wholly owned directly by His Majesty in right of Canada or a province;

- (g) head of a government agency;

- (h) judge of an appellate court in a province, the Federal Court of Appeal or the Supreme Court of Canada;

- (i) leader or president of a political party represented in a legislature;

- (j) holder of any prescribed office or position; or

- (k) mayor, reeve or other similar chief officer of a municipal or local government.

Reference:

PCMLTFA, S.C. 2000, c 17, s. 9.3(3).- Politically exposed foreign person

A person who holds or has held one of the following offices or positions in or on behalf of a foreign state:

- (a) head of state or head of government;

- (b) member of the executive council of government or member of a legislature;

- (c) deputy minister or equivalent rank;

- (d) ambassador, or attaché or counsellor of an ambassador;

- (e) military officer with a rank of general or above;

- (f) president of a state-owned company or a state-owned bank;

- (g) head of a government agency;

- (h) judge of a supreme court, constitutional court or other court of last resort;

- (i) leader or president of a political party represented in a legislature; or

- (j) holder of any prescribed office or position.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Possibility

In regards to completing a suspicious transaction report (STR), the likelihood that a transaction may be related to a money laundering/terrorist financing (ML/TF) offence. For example, based on your assessment of facts, context and ML/TF indicators you have reasonable grounds to suspect that a transaction is related to the commission or attempted commission of an ML/TF offence. (possibilité)

- Precious metal

Gold, silver, palladium or platinum in the form of coins, bars, ingots or granules or in any other similar form. (métal précieux)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Precious stones

Diamonds, sapphires, emeralds, tanzanite, rubies or alexandrite. (pierre précieuse)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Prepaid payment product

A product that is issued by a financial entity and that enables a person or entity to engage in a transaction by giving them electronic access to funds or virtual currency paid to a prepaid payment product account held with the financial entity in advance of the transaction. It excludes a product that:

- (a) enables a person or entity to access a credit or debit account or one that is issued for use only with particular merchants; or

- (b) is issued for single use for the purposes of a retail rebate program.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Prepaid payment product account

An account – other than an account to which only a public body or, if doing so for the purposes of humanitarian aid, a registered charity as defined in subsection 248(1) of the Income Tax Act, can add funds or virtual currency – that is connected to a prepaid payment product and that permits:

- (a) funds or virtual currency that total $1,000 or more to be added to the account within a 24-hour period; or

- (b) a balance of funds or virtual currency of $1,000 or more to be maintained.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Prescribed

Prescribed by regulations made by the Governor in Council. (Version anglaise seulement)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Probability

The likelihood in regards to completing a suspicious transaction report (STR) that a financial transaction is related to a money laundering/terrorist financing (ML/TF) offence. For example, based on facts, having reasonable grounds to believe that a transaction is probably related to the commission or attempted commission of an ML/TF offence. (probabilité)

- Production order

A judicial order that compels a person or entity to disclose records to peace officers or public officers. (ordonnance de communication)

- Public body

Means

- (a) a department or an agent of His Majesty in right of Canada or an agent or mandatary of His Majesty in right of a province;

- (b) an incorporated city or town, village, metropolitan authority, township, district, county, rural municipality or other incorporated municipal body in Canada or an agent or mandatary in Canada of any of them; and

- (c) an organization that operates a public hospital and that is designated by the Minister of National Revenue as a hospital authority under the Excise Tax Act, or an agent or mandatary of such an organization.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Real estate broker or sales representative

A person or entity that is authorized under provincial legislation to act as an agent or mandatary for purchasers or vendors in respect of the purchase or sale of real property or immovables. (courtier ou agent immobilier)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Real estate developer

A person or entity that, in any calendar year after 2007, has sold to the public, other than in the capacity of a real estate broker or sales representative:

- (a) five or more new houses or condominium units;

- (b) one or more new commercial or industrial buildings; or

- (c) one or more new multi-unit residential buildings each of which contains five or more residential units, or two or more new multi-unit residential buildings that together contain five or more residential units.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Reasonable measures

Steps taken to achieve a desired outcome, even if they do not result in the desired outcome. For example, this can include doing one or more of the following:

- asking the client,

- conducting open source searches,

- retrieving information already available, including information held in non-digital formats, or

- consulting commercially available information.

- Receipt of funds record

A record that indicates the receipt of an amount of funds and that contains the following information:

- (a) the date of the receipt;

- (b) if the amount is received from a person, their name, address and date of birth and the nature of their principal business or their occupation;

- (c) if the amount is received from or on behalf of an entity, the entity's name and address and the nature of their principal business;

- (d) the amount of the funds received and of any part of the funds that is received in cash;

- (e) the method by which the amount is received;

- (f) the type and amount of each fiat currency involved in the receipt;

- (g) if applicable, the exchange rates used and their source;

- (h) the number of every account that is affected by the transaction in which the receipt occurs, the type of account and the name of each account holder;

- (i) the name and address of every other person or entity that is involved in the transaction, the nature of their principal business or their occupation and, in the case of a person, their date of birth;

- (j) every reference number that is connected to the transaction and has a function equivalent to that of an account number; and

- (k) the purpose of the transaction.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Registered pension plan

Has the same meaning as in subsection 248(1) of the Income Tax Act. (régime de pension agréé)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Registered retirement income fund

Has the same meaning as in subsection 248(1) of the Income Tax Act. (fonds enregistré de revenu de retraite)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Reliable

In respect of information that is used to verify identity, means that the source is well known, reputable, and is considered one that you trust to verify the identity of the client. (fiable)

- Representative for service

An individual in Canada that has been appointed by a person or entity that is a foreign money services business (FMSB), pursuant to the PCMLTFA, to receive notices and documents on behalf of the FMSB. (représentant du service)

- Risk assessment

The review and documentation of potential money laundering/terrorist financing risks in order to help a business establish policies, procedures and controls to detect and mitigate these risks and their impact. (évaluation des risques)

- Securities dealer

A person or entity that is referred to in paragraph 5(g) of the Act. (courtier en valeurs mobilières)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Senior officer

In respect of an entity, means:

- (a) a director of the entity who is one of its full-time employees;

- (b) the entity's chief executive officer, chief operating officer, president, secretary, treasurer, controller, chief financial officer, chief accountant, chief auditor or chief actuary, or any person who performs any of those functions; or

- (c) any other officer who reports directly to the entity's board of directors, chief executive officer or chief operating officer.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Service agreement

An agreement between a money services business (MSB) and an organization according to which the MSB will provide any of the following MSB services on an ongoing basis:

- money transfers;

- foreign currency exchange;

- issuing or redeeming money orders, traveller's cheques or anything similar; or

- dealing in virtual currencies.

- Settlor

A settlor is an individual or entity that creates a trust with a written trust declaration. The settlor ensures that legal responsibility for the trust is given to a trustee and that the trustee is provided with a trust instrument document that explains how the trust is to be used for the beneficiaries. A settlor includes any individual or entity that contributes financially to that trust, either directly or indirectly. (constituant)

- Shell bank

A foreign financial institution that:

- (a) does not have a place of business that:

- (i) is located at a fixed address—where it employs one or more persons on a full-time basis and maintains operating records related to its banking activities—in a country in which it is authorized to conduct banking activities; and

- (ii) is subject to inspection by the regulatory authority that licensed it to conduct banking activities; and

- (b) is not controlled by, or under common control with, a depository institution, credit union or foreign financial institution that maintains a place of business referred to in paragraph (a) in Canada or in a foreign country.

Reference:

PCMLTFR, SOR/2002-184, s. 1(1).- (a) does not have a place of business that:

- Signature

Includes an electronic signature or other information in electronic form that is created or adopted by a client of a person or entity referred to in section 5 of the Act and that is accepted by the person or entity as being unique to that client. (signature)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Signature card

In respect of an account, means a document that is signed by a person who is authorized to give instructions in respect of the account, or electronic data that constitutes the signature of such a person. (fiche-signature)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Source

The issuer or provider of information or documents for verifying identification. (source)

- Source of funds or of virtual currency (VC)

The origin of the particular funds or VC used to carry out a specific transaction or to attempt to carry out a transaction. It is how the funds were acquired, not where the funds may have been transferred from. For example, the source of funds could originate from activities or occurrences such as employment income, gifts, the sale of a large asset, criminal activity, etc. (origine des fonds ou de la monnaie virtuelle (MV))

- Source of wealth

The origin of a person's total assets that can be reasonably explained, rather than what might be expected. For example, a person's wealth could originate from an accumulation of activities and occurrences such as business undertakings, family estates, previous and current employment income, investments, real estate, inheritance, lottery winnings, etc. (origine de la richesse)

- Starting action

With respect to a reportable transaction, information related to the instructions provided by the person or entity making the request to the reporting entity to start a transaction. For example, an individual arrives at a bank and requests to purchase a bank draft. The starting action is the details of the instructions for the purchase which includes the funds or virtual currency that the requesting person or entity brought to the reporting entity. A transaction must have at least one starting action. (action d’amorce)

- SWIFT

The Society for Worldwide Interbank Financial Telecommunication. (SWIFT)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Terrorist activity

Has the same meaning as in subsection 83.01(1) of the Criminal Code. (activité terroriste)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Terrorist activity financing offence

An offence under section 83.02, 83.03 or 83.04 of the Criminal Code or an offence under section 83.12 of the Criminal Code arising out of a contravention of section 83.08 of that Act.

A terrorist financing offence is knowingly collecting or giving property (such as money) to carry out terrorist activities. This includes the use and possession of any property to help carry out the terrorist activities. The money earned for terrorist financing can be from legal sources, such as personal donations and profits from a business or charitable organization or from criminal sources, such as the drug trade, the smuggling of weapons and other goods, fraud, kidnapping and extortion. (infraction de financement des activités terroristes)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Third party

Any individual or entity that instructs another individual or entity to act on their behalf for a financial activity or transaction. (tiers)

- Threats to the security of Canada

Has the same meaning as in section 2 of the Canadian Security Intelligence Service Act. (menaces envers la sécurité du Canada)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Training program

A written and implemented program outlining the ongoing training for your employees, agents or other individuals authorized to act on your behalf. It should contain information about all your obligations and requirements to be fulfilled under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act and its associated Regulations. (programme de formation)

- Trust

A right of property held by one individual or entity (a trustee) for the benefit of another individual or entity (a beneficiary). (fiducie)

- Trust company

A company that is referred to in any of paragraphs 5(d) to (e.1) of the Act. (société de fiducie)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Trustee

A trustee is the individual or entity authorized to hold or administer the assets of a trust. (fiduciaire)

- Tutor

In the context of civil law, a person who has been lawfully appointed to the care of the person and property of a minor. (tuteur)

- Two year effectiveness review

A review, conducted every two years (at a minimum), by an internal or external auditor to test the effectiveness of your policies and procedures, risk assessment, and training program. (examen bisannuel de l'efficacité)

- Valid

In respect of a document or information that is used to verify identity, appears legitimate or authentic and does not appear to have been altered or had any information redacted. The information must also be valid according to the issuer, for example if a passport is invalid because of a name change, it is not valid for FINTRAC purposes. (valide)

- Verify identity

To refer to certain information or documentation, in accordance with the prescribed methods, to identify a person or entity (client). (vérifier l'identité)

- Very large corporation or trust

A corporation or trust that has minimum net assets of $75 million CAD on its last audited balance sheet. The corporation's shares or units have to be traded on a Canadian stock exchange or on a stock exchange designated under subsection 262(1) of the Income Tax Act. The corporation or trust also has to operate in a country that is a member of the Financial Action Task Force (FATF). (personne morale ou fiducie dont l'actif est très important)

- Violation

A contravention of the Act or the regulations that is designated as a violation by regulations made under subsection 73.1(1). (violation)

Reference:

PCMLTFA, S.C. 2000, c 17, s. 2(1).- Virtual currency

Means:

- (a) a digital representation of value that can be used for payment or investment purposes that is not a fiat currency and that can be readily exchanged for funds or for another virtual currency that can be readily exchanged for funds; or

- (b) a private key of a cryptographic system that enables a person or entity to have access to a digital representation of value referred to in paragraph (a).

Reference:

PCMLTFR, SOR/2002-184, s. 1(2) and PCMLTFSTRR, SOR/2001-317, s. 1(2).- Virtual currency exchange transaction

An exchange, at the request of another person or entity, of virtual currency for funds, funds for virtual currency or one virtual currency for another. (opération de change en monnaie virtuelle)

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Virtual currency exchange transaction ticket

A record respecting a virtual currency exchange transaction—including an entry in a transaction register—that sets out:

- (a) the date of the transaction;

- (b) in the case of a transaction of $1,000 or more, the name and address of the person or entity that requests the exchange, the nature of their principal business or their occupation and, in the case of a person, their date of birth;

- (c) the type and amount of each type of funds and each of the virtual currencies involved in the payment made and received by the person or entity that requests the exchange;

- (d) the method by which the payment is made and received;

- (e) the exchange rates used and their source;

- (f) the number of every account that is affected by the transaction, the type of account and the name of each account holder;

- (g) every reference number that is connected to the transaction and has a function equivalent to that of an account number; and

- (h) every transaction identifier, including the sending and receiving addresses.

Reference:

PCMLTFR, SOR/2002-184, s. 1(2).- Working days

In respect of an electronic funds transfer (EFT) report or a large virtual currency transaction report, a working day is a day between and including Monday to Friday. It excludes Saturday, Sunday, and a public holiday. (jour ouvrable)

- Date Modified: